12 Temmuz 2014 Cumartesi

11 Temmuz 2014 Cuma

Supply and Demand

We'll talk about competitive market, supply and demand model and curves.

A competitive market is a market in which there are many sellers and buyers. when a market is competitive,its behaviour is well described by a model known as the supply and model.There are five key elements in this model:

- The demand curve

- the supply curve

- the set of factors that cause the demand curve to shift and the set of factors that cause the supply curve to shift.

- the equilibrium price

- the way the equilibrium price changes when the supply or demand curves shift

THE DEMAND CURVE

A demand curve is a graphical represantation of the demand schedule.It shows how much of a good or service consumers want to buy at any given price.The Law of demand says that higher price for a good ,other things equal,leads people to demand a smaller quantitiy of the good.

SHİFTS OF THE DEMAND CURVE

Any event that increases demand shifts the demand curve to the right,reflecting a rise in the quantitiy demanded at any given price.Any event that decreases demand shifts the demand curve to the left,reflecting a fall in the quantity demanded at any given price.

*economists believe that there are 4 principal factors that shift the demand curve for a good:

- changes in the prices of related goods

- changes in income

- changes in tastes

- chanes in expectations

*two goods are substitues if a fall in the price of one of the goods makes consumers less willing to buy the other good.

*two goods are complements if a fall in the price of one good makes people more willing to buy the other good.

THE SUPPLY CURVE

A supply curve shows graphically how much of a good or service people are willing to sell at any given price.

Economists believe that shifts of supply curves are mainly the result of three factors

- changes in input prices

- changes in technology

- changes in expectations

Any event that increases supply shifts the supply curve to the right,reflecting a rise in the quantitiy supplied at any given price.Any event that decreases supply shifts the supply curve to the left,reflecting a fall in the quantitiy supplied at any given price.

EQUİLİBRİUM

A competitive market is in equilibrium when price has moved to a level at which the quantitiy demanded of a good equals the quantity supplied of that good.The price at which this takes place is the equilibrium price,also referred to as the market-clearing price.The quantitiy of the good bought and sold at that price is the equilibrium quantity.

Equilibrium and Shifts of the Demand Curve

An increase in demand shifts demand curve to the right and at new equilibrium point price and quantitiy would be higher.

Equilibrium and Shifts of the Supply curve

An increase in supply shifts supply curve to the right.At new equilibrium point price would be lower,and quantity would be higher.

PRİCE CONTROL

Price controls are legal restrictions on how high or low a market price may go.They can take two forms. a price ceiling, or a price floor.

Price ceiling: A maximum price sellers are aloowed to charge for a good

Price floor: A minimum price buyers are required to pay for a good.

Effects of Price Ceiling

price ceilings often leads to inefficiency in the form of inefficient allocation to consumers.

Effects of Price Floors

10 Temmuz 2014 Perşembe

Economic Models

In this chapter,we will look at three economic models that are crucially important in their own right and also illustrate why such models are so useful.

The idea behind this model is to improve our understanding of trade-offs by considering a simplified economy that produces only two goods.This simplification enables us to show the trade off graphically.

The idea behind this model is to improve our understanding of trade-offs by considering a simplified economy that produces only two goods.This simplification enables us to show the trade off graphically.

The hit movie Cast Away, starring Tom Hanks, was an update of the classic story of Robinson Crusoe.As in the original story of Robinson Crusoe,the character played by Hanks had limited resources:the natural resources of the island, a few items he managed to salvage from the plane,and of course his own time and effor.With only this resources,he had to make life.

As a result, any economy-wheter it contains only one man- faces trade-offs.For example if he devotes resources to cach fish,he can't use these same resources to gather coconut.Economists use the model known as Production Possibility Frontier.

Economists believe that opportunity costs are usually increases.The reason is that when only a small amount of good is produced ,the economy can use resources that are especially well suited for that production.

Economic Growth

We define economic growth as the growing ability of the economy to produce goods and services. ıt results in an outward shifft of the production possibility frontier because production possibilities are expanded.The economy can now produce more of everything.For example,if production is initially at point A, it could move to point e.

1. Production Possibility Frontier

The idea behind this model is to improve our understanding of trade-offs by considering a simplified economy that produces only two goods.This simplification enables us to show the trade off graphically.

The idea behind this model is to improve our understanding of trade-offs by considering a simplified economy that produces only two goods.This simplification enables us to show the trade off graphically.The hit movie Cast Away, starring Tom Hanks, was an update of the classic story of Robinson Crusoe.As in the original story of Robinson Crusoe,the character played by Hanks had limited resources:the natural resources of the island, a few items he managed to salvage from the plane,and of course his own time and effor.With only this resources,he had to make life.

As a result, any economy-wheter it contains only one man- faces trade-offs.For example if he devotes resources to cach fish,he can't use these same resources to gather coconut.Economists use the model known as Production Possibility Frontier.

It shows the maximum quantitiy of one good that can be produced given the quantitiy of the another good produced. Feasible production is shown by the area inside or on the curve.Production at point x is feasible but not efficient.Point A,B,C are feasible and efficient, but point Y is not feasible.

INCREASING OPPORTİNİTY COST

We define economic growth as the growing ability of the economy to produce goods and services. ıt results in an outward shifft of the production possibility frontier because production possibilities are expanded.The economy can now produce more of everything.For example,if production is initially at point A, it could move to point e.

2.Comparative Advantage and Gain from Trade

An individual has a comparative advantage in producing a good or service if the opprtunity cost of producing the good is loweer for that individual than for other people. The model provides a clear illustration of the gains from trade:by aggreing to specialize and provide goods to each other, the castaway can produce more and therefore both be better off than if they tried to be self-sufficient.

Positive economics: is the branch of economic analyses that describes the way the economy actually works.

Normative Economics: makes prescriptions about the way the economy should work.

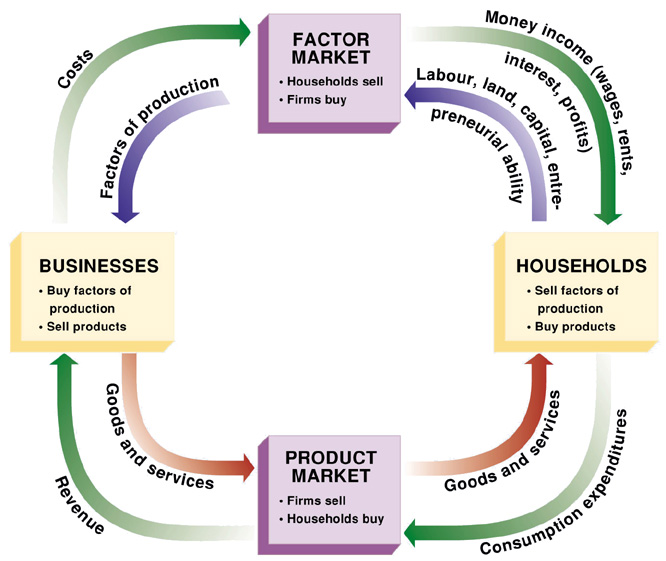

3.The Circular-flow Diagram

The circular flow diagram is a mod

el that represents the transactions in an economy by flows around a circle.This model contains only two kinds of inhabitants: household and firms.

The model represents the flows of money and goods and services in the economy.In the markets for goods and services households purchase goods and services from firms,generating a flow of money to the firms and flow of goods and services to the households.The money flows back to households as firms purchase factors of production from the household in factor markets.

Positive vs. Normative Economics

Positive economics: is the branch of economic analyses that describes the way the economy actually works.

Normative Economics: makes prescriptions about the way the economy should work.

When and Why Economists Disagree?

Economists disagree for two main reasons.One,they may disagree about which simplifications to make in a model.Two,economists may disagree about values.9 Temmuz 2014 Çarşamba

Introduction to Economics: First Principles

There are some key terms in economics. Let me explain them.

Economy: is a system for coordinating society's productive activities.

Economics: is the study of economies,at the level both of of individuals and society as a whole.

Market Economy: is an economy in which decisions about production and consumption are made by individual producers and consumers.

*the alternative to a market economy is a command economy, in which there is a central authority making decisions about production and consumption.they have been tried,most notably in the soviet union between 1917-1991.But they didn't work.

Invisible Hand: refers to the way in which the individual pursuit of self interest can lead to good results for society as a whole.

Microeconomics: is the branch of economics that studies how people make decisions and how this decisions interact.

*One of the key themes in microeconomics is the validity of Adam Smith's insight: Individiuals pursuing their own interests often do promote the interest of socety as a whole.

Market Failure: when the individual pursuit of self interest leads to bad results for society as a whole,there is market failure.

Recession: is a downturn in the ecoonomy

Economic Growth: is growing ability of the economy to produce goods and services.

Macroeconomics: is the branch of economics that is concerned with overall ups and downs in the economy.

These keywords are important to understand the core of economics.

now, we can go on with FİRST PRİNCİPLES:

*We will learn a set of principles for understanding the economics of how individuals make choices and how individuals choices interact.

*Individual Choice: is the decision by an individual of what to do,which necessarily involves a decision of what not to do.

FİRST PRİNCİPLES

- Resources Are Scarce: The fact is you can't always get what you want.So; you must make choices.Limited income and time are things that keep people from having everything they wantA resource is anything that can be used to produce something else. List of the economy's resources usually begin with land,labor,capital,human capital.A resource is scarce when quantity of the resource available is not large enough to satisfy all productive uses.There are many scarce resources like natural resources,it includes,minerals,lumber,petroleum etc. there is also limited quantity of human resources:labor, skill and intelligence.

2.Opportinity Cost: the real cost of something is what you must give up to get it. The concept of opportinity cost is crucial to understanding individual consumer choice, because in the end, all costs are opportinity cost.

3. "How Much?" is a decision at the Margin: if you are taking both economics and chemistry in this semester, you must decide how much time to spend studying for each.when it comes to understanding how much decisions economcs has an important insight to offer: how much is a decision at the margin.you make a trade-off when you compare the costs with the benefits of doing something. Decisions about whether to do a bit more or a bit less of an activity are marginal decisions.the study of such decisions is known marginal analysis.

4. People Usually Exploit Opportunuties to Make Themselves Better Off:

In fact,the principle that people will exploit opportunities to make themselves better off is the basis of all predictions by economists abut individual behaviour.

When changes in the available opportunities offer rewards to those who change their behaviour,we say that people face new incentives.

*An incentive is anything that offers rewards to people who change their behaviour.

*There are gains from trade: people can get more of what they want through trade than they could if they tried to be self-suffiicient.This increase in output is due to specialization.

*Specialization: each person specializes in the task that he or she is good at performing.- Resources Are Scarce: The fact is you can't always get what you want.So; you must make choices.Limited income and time are things that keep people from having everything they wantA resource is anything that can be used to produce something else. List of the economy's resources usually begin with land,labor,capital,human capital.A resource is scarce when quantity of the resource available is not large enough to satisfy all productive uses.There are many scarce resources like natural resources,it includes,minerals,lumber,petroleum etc. there is also limited quantity of human resources:labor, skill and intelligence.

3. "How Much?" is a decision at the Margin: if you are taking both economics and chemistry in this semester, you must decide how much time to spend studying for each.when it comes to understanding how much decisions economcs has an important insight to offer: how much is a decision at the margin.you make a trade-off when you compare the costs with the benefits of doing something. Decisions about whether to do a bit more or a bit less of an activity are marginal decisions.the study of such decisions is known marginal analysis.

When changes in the available opportunities offer rewards to those who change their behaviour,we say that people face new incentives.

*An incentive is anything that offers rewards to people who change their behaviour.

*There are gains from trade: people can get more of what they want through trade than they could if they tried to be self-suffiicient.This increase in output is due to specialization.

Market Move Toward Equilibrium

*An economic situation is in equilibrium when no individual would be better off doing something different.

*An economy is efficient if it takes all opportunities to make some people better off without making other people worse off.

Kaydol:

Yorumlar (Atom)